What does 2026 hold? Preparing for the year ahead

We look back at 2025 and consider the key governance and risk issues that tax leaders must address in 2026.

Key Points

What is the issue?

After a turbulent 2025, tax leaders face continued uncertainty, tougher enforcement and rising global compliance demands as they prepare for 2026.

What does it mean to me?

Greater scrutiny from HMRC, expanding international obligations and accelerating use of technology mean that tax governance and risk management can no longer be informal or reactive.

What can I take away?

Success in 2026 will depend on embedding robust tax control frameworks, clear accountability and resilient operating models that can endure ongoing change.

The year 2025 was one of tough fiscal choices and global disruption. In the UK, the Budget was the most obvious focal point – and one of the most anticipated in recent years. It was presented as a careful balance between fairness and fiscal discipline, and it elicited mixed responses.

Supporters emphasised stability and predictability, highlighting the increased fiscal headroom as a sign of resilience that would encourage business investment. Critics, however, viewed the Budget as cautious and lacking ambition, arguing that it amounted to careful tinkering rather than transformative reform. The Institute for Fiscal Studies (IFS) praised the creation of fiscal headroom as ‘sensible’, but stressed that this was ‘not a grand tax-reforming Budget’ and showed ‘no real appetite for using tax reform to boost growth’.

Confidence improved – but uncertainty remains

Last year, I wrote in Tax Adviser that as we hit 2025, ‘uncertainty was going to move to a greater confidence over future tax stability’. In advance of writing this article, I tested this assertion using an AI assistant. Its answer was non‑committal – and perhaps rightly so.

On one hand, confidence has improved. The government has tried to outline a clearer medium-term strategy and has avoided some of the more drastic measures that had been anticipated. However, uncertainty remains. Many changes have been deferred, fiscal drag continues to play a significant role, and businesses and individuals still face unpredictability in their actual tax burdens. This is compounded by ongoing political instability and wider global volatility.

In this article, I argue that while 2025 brought some progress towards clarity, uncertainty still lingers. Looking ahead to 2026, the message is that businesses and individuals should remain agile, monitor risks and strengthen their tax governance. The signs point to calmer waters, but resilience and adaptability remain essential.

Enforcement takes centre stage

One prediction from last year’s article did prove accurate: that in 2025 ‘we will see the first prosecution under the Corporate Criminal Offence (CCO)’. This indeed materialised in August, involving an alleged R&D tax credit repayment fraud, finally addressing years of criticism that the CCO regime lacked teeth.

This prosecution is likely to set the tone for tougher enforcement and coincided with the introduction of the UK’s new Failure to Prevent Fraud offence in September 2025. This further expanded corporate liability for economic crime and prompted many organisations to refresh their CCO procedures, integrating fraud and tax evasion prevention into a single control environment. The message from HMRC in 2025 was clear: enforcement is real, and prevention frameworks must be demonstrable and robust.

Global pressures and operational strain

Internationally, businesses continue to navigate the compliance challenges of Pillar Two, investing in data, systems and processes to meet minimum tax requirements across multiple jurisdictions. Changes in trade and tariffs are continuing to disrupt supply chains and tax planning strategies. I am sure the volatility of tariff adjustments, particularly in the early months of 2025, remains fresh in many memories.

Global tax teams also reported mounting operational pressures. BDO’s Global Tax Outlook, which surveyed 500 global tax leaders during the summer of 2025, found that 66% of businesses expected tax compliance costs to rise. Meanwhile, 81% reported increased time spent responding to tax authority queries, with some teams spending around a quarter of their time on that alone. The drive for efficiency led 62% of organisations to increase training, 56% to upgrade technology, and 47% to expand outsourcing.

Changes in compliance and other tax law also emerged as a central theme in the survey, with half of businesses citing ‘keeping up with regulations’ as their biggest challenge. Yet while the pace and complexity of regulatory change can feel daunting, it need not be a burden. Proactive compliance strategies and the effective use of technology can turn regulatory demands into opportunities for improved efficiency, stronger governance and competitive advantage.

As highlighted in the Global Tax Outlook, best practice is no longer about box-ticking; it is about building an integrated, risk-aware compliance model that can withstand deeper scrutiny.

Strategic imperatives in 2026

As we move into 2026, the hope is for greater resilience. This requires a proactive, future-ready tax operating model – one that is not only compliant but also flexible enough to adapt to evolving regulations and emerging business challenges. A truly robust tax function integrates risk management, embraces technology and fosters collaboration across the organisation, ensuring it can respond confidently to whatever the regulatory landscape and political shifts bring next.

Businesses are taking steps. According to BDO’s Global Tax Outlook, most organisations report having a tax risk framework in place, although maturity varies. While 56% describe their framework as comprehensive, 46% say it remains informal or in development. Among the 500 global tax directors surveyed, comprehensive frameworks include monitoring and review processes (71%), documented policies (61%), AI (52%), risk assessment (50%) and escalation workflows (48%). Informal frameworks, by contrast, lean heavily on ad-hoc practices.

Tax authorities increasingly expect a ‘no surprises’ culture. In the UK, HMRC continues to promote cooperative compliance, signalling that effective tax control frameworks and strong governance are central to lighter-touch oversight.

At BDO, we saw a notable increase in Business Risk Review assessments in 2025, reflecting their role as a cornerstone of HMRC’s approach to evaluating large businesses. Business Risk Reviews provide a structured, forward-looking dialogue between HMRC and taxpayers, focusing on the effectiveness of tax governance, risk management and the robustness of internal controls. A positive outcome can lead to a lower risk rating, which in turn means fewer interventions and a more collaborative relationship with HMRC. Conversely, gaps in documentation, unclear processes or reactive compliance can result in a higher risk rating and increased scrutiny.

Emerging audit-led initiatives

We are also aware that HMRC is seeking to introduce a new audit-led programme targeting how large businesses manage and generate their tax positions. Initially targeting the automotive, retail and insurance sectors, this involves multi‑day onsite assessments focused on governance, controls and data flows across key tax areas. Businesses must provide detailed evidence of how new entities are integrated into tax processes, with particular emphasis on control effectiveness and accountability.

Proactive preparation for this initiative strengthens compliance with Senior Accounting Officer and Business Risk Review requirements, and demonstrates a commitment to transparency and best practice. As HMRC promotes cooperative compliance, the new programme reinforces the need for robust tax control frameworks and proactive risk management. No doubt we will hear more about this in due course.

In the meantime, for organisations impacted by a Business Risk Review, this is not just a compliance exercise but also an opportunity to demonstrate transparency and commitment to best practice. Regular internal reviews, clear documentation of tax processes and evidence of proactive risk management are all critical to achieving a favourable outcome. By treating the Business Risk Review as a chance to showcase a mature tax control framework – rather than a box-ticking exercise – businesses can build trust with HMRC, securing the benefits of lighter-touch oversight and greater certainty.

Aneeta Samra, Tax Director at Sotheby’s, captures this well: ‘A strong Business Risk Review outcome is earned by everyday behaviours – complete records, timely responses and a good working relationship with HMRC. Our aim is simple: ensure we have strong tax governance and a robust tax risk framework which complements and reflects internal communication – so HMRC has confidence that we proactively identify tax issues as they arise and that they don’t linger.’

2026: from transformation to endurance

When I spoke to Miranda Chamberlain, Head of Tax at Mace, at the start of 2025, she described the year ahead as bringing ‘Winds of Change’ – a fitting reference, as 2025 was the Chinese Year of the Snake, symbolising transformation. As she observed last year: ‘The tax director must be able to robustly demonstrate a responsible tax agenda providing certainty in a climate of uncertainty.’

Looking ahead, 2026 is the Year of the Horse and sets an apt tone: it calls for disciplined execution and sustained effort. With greater stability, tax leaders can take stock, consolidate plans and build the confidence needed to future proof their tax functions.

As Miranda says: ‘A strong compliance model underpinned by clear accountability, reliable data and regular assurance – embedded in the culture of a business – creates an environment of predictability, certainty and true transparency, supporting long-term business decisions even as the external environment continues to evolve.’

Paul Whiteley, Group Head of Tax at LEK Consulting, reinforces the central element of a strong compliance model, namely management of tax risk. He reminds us that most tax risk arises not within tax or finance teams but from the wider business. It is therefore critical to ensure that everyone understands the significance of tax risk, the impact it can have on the business and the need to manage it properly: ‘That goes across not just people who have tax responsibilities, but people in the broader business.’

As 2026 unfolds, tax leaders must consolidate their strategies and embed robust, risk-aware operating models. Clear accountability, reliable data and regular assurance will be key to building resilience and supporting long-term decisions. Ultimately, managing tax risk is a collective responsibility across the business, ensuring stability and confidence in an ever-evolving environment.

Corporate Tax Roadmap

Last year, I highlighted the importance of the Corporate Tax Roadmap 2024. While not front-page news, it remains relevant as it sets out the government’s plans for corporation tax – offering a welcome level of predictability for corporates and setting out the government’s intention to keep corporation tax policy stable and attractive for investment.

The roadmap confirmed that key elements – such as the headline corporation tax rate, current R&D relief rates and the core capital allowance structure – would remain unchanged. It also identified areas for potential reform, including providing advance certainty for major projects, expanding R&D clearances, updating international tax rules, reviewing land remediation relief, and examining the tax treatment of pre-development costs.

Several consultations on these topics took place in 2025. The Advance Tax Certainty Service is due to launch in July 2026, with a pilot on R&D certainty for SMEs planned for the Spring, although some elements – including the review of pre-development costs – have been postponed.

International issues: Pillar Two

Pillar Two remains a central workload driver. Many groups invested heavily in 2025 to collect new data points, upgrade systems and revisit global tax operating models. This continues into 2026, alongside ongoing geopolitical uncertainty around trade, tariffs and US tax reform.

As Ross Robertson, one of our Corporate International Tax partners at BDO UK, reminded me, ‘the devil is in the detail’. The Pillar Two journey is far from a box-ticking exercise. Businesses must undertake detailed reviews of their structures and processes to ensure compliance and avoid costly assumptions.

The cost implications are real. Ralf Pieters, Head of Tax at AkzoNobel, explains in the Global Tax Outlook that: ‘There was no doubt that a solution [for Pillar Two] would require quite an upfront investment, as would upskilling and perhaps adding resources to the team.’ Instead, his organisation opted for outsourcing after recognising the scale of investment required – a decision that proved more cost-effective than initially expected.

This experience highlights a broader trend. Cost considerations often drive initial decisions, and the complexity of Pillar Two is prompting organisations to rethink their approach. Ian Bowden, who leads BDO’s Pillar Two technology implementation, says: ‘Pillar Two represents a significant data challenge, providing tax and finance teams with a compelling business case for transformation.

‘Many groups are leveraging the Pillar Two requirements to drive broader changes within their organisations, particularly in the tax provision process. The interconnected nature of data has compelled groups to adopt a holistic view of their tax function operations, fostering comprehensive improvements and strategic advancements.’

The challenge – and opportunity – of AI

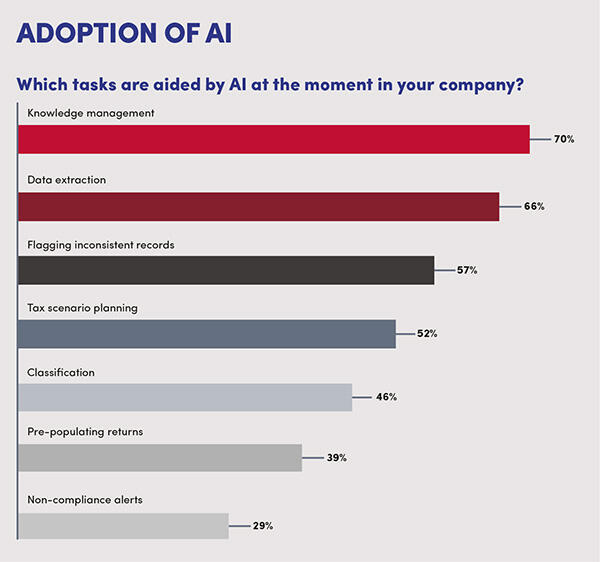

Technology, and particularly AI, will be a defining topic for 2026. BDO’s survey shows that AI is no longer a future concept – it’s already embedded in key processes: knowledge management (70%), data extraction (66%), flagging inconsistent records (57%) and tax scenario planning (52%). The immediate benefits are clear: faster turnaround times, improved data accuracy and easier access to knowledge.

The bigger question, however, is how prepared we are for AI to move beyond operational efficiency and start shaping strategic decisions. What does it mean when algorithms begin influencing judgement calls traditionally reserved for human expertise?

In 2025, the jump in the use of AI tools has been significant, and by the end of 2026 we may find ourselves operating in a very different landscape altogether. As we adopt AI, it’s crucial to think about governance, ethical frameworks and the skills to interpret AI-driven results for tax purposes. Are our organisations prepared to trust AI as a strategic adviser, not just an assistant? If so, how do we ensure transparency, accountability and alignment with our tax values?

Conclusion

As we move into 2026, the focus and hope for all tax professionals is to move from transformation and uncertainty to endurance. The turbulence of recent years has reinforced the need for resilience, robust governance and proactive risk management. With enforcement and HMRC scrutiny tightening, regulatory complexity increasing and technology – particularly AI – becoming integral to our everyday lives, organisations must embed robust tax operating models supported by reliable data and clear accountability, rather than relying on reactive solutions.

Success will depend on collaboration across the business, disciplined execution and a commitment to transparency. In an environment that remains unpredictable, endurance is not about standing still – it’s about navigating change while supporting long-term strategic tax governance.

© Getty images

—

Source: https://www.taxadvisermagazine.com/article/what-does-2026-hold-preparing-year-ahead

Responses